Informed Consumer Project

The purpose of this project was to become a more informed consumer and educate others about what we learned. We all chose a topic to research and formulated 6 questions about that topic. Mine was on health insurance. Because I couldn't find any equations or formulas on how to calculate insurance, I just created situational questions. They didn't consist of any difficult equations or very hard problem solving. Since there were no formulas for me to use, I came up with three other questions just calculating loans and using a formula that dealt with monthly payments, interest and debt.

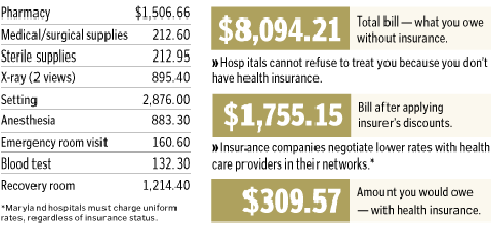

Health Insurance

You’re married and your spouse is in the military but is soon going to be discharged, in 4 months. You’re planning on having a child and are deciding to go with term or whole life health insurance. Neither of you have health insurance but are most likely going to go with TRICARE. The annual deductibles for individuals in active duty is $150 and $300 for families. The maximum annual out-of-pocket amount is $1000. You don’t have to pay any enrollment fees if your spouse is still in active duty. You’re not planning on having a baby for at least another year, but still have to get the family plan.

1. If you decide to get the family plan and continue with it for 25 years, how much will you pay monthly? How much will you have paid total?

$25/month

$25*12*25= $7500

2. Say you didn’t get any health insurance because both you and your spouse never had any medical issues in either of your families. But 7 years after your married, you have 2 kids and one breaks their arm during soccer practice. No insurance but you have been putting $100 in savings every month for the past 6 years. The cost of the hospitalization and care for your child totals to $4,200.

Is the amount you have saved enough to pay for the cost? How much in savings will you have left over after the cost is paid?

Yes.

You will have $3,000 left over.

3. Say you did have insurance, but Tricare only covered the cost of x-rays, ER visit, medical treatment, setting, and pharmacy. These are the most expensive costs when it comes to fixing a broken bone. They account for 80% of the total expense.

How much would they cover and how much would you have to pay for?

.8*4200=3360

They would cover $3,360.

.2*4200=840

You would still have to pay $840

Loans

2. Susy wants to buy a car that costs $37,000. She puts a down payment of $5,000. To pay for the rest Susy takes out a loan of $32,000, it’s a 10 year loan with an APR of 6%.

a. How much will she be paying a month?

$355.27

$10,632.40 in interest

b. If she pays an extra $65 how many months will it take her to pay that off?

420.27= .06/12(32,000)

1-(.06/12+1)^-n

420.27(1-(.06/12+1)^-n)= 160

1-(1+.06/12)^-n= 0.38

-0.62=-(1+.06/12)^-n

-.62= -.005^-n

n(-.62)= n(-1.005^-n)

ln(0.62)= -n(ln1.005)

ln(0.62) = -n

ln(1.005)

-95.8=n

It will take her roughly 95.8 months to pay it off.

c. How much interest does she save if she pays the extra money?

$8,261.87 in interest

10632.4-8,261.87=2,370.53

She saves $2,370.53 in interest.

You’re married and your spouse is in the military but is soon going to be discharged, in 4 months. You’re planning on having a child and are deciding to go with term or whole life health insurance. Neither of you have health insurance but are most likely going to go with TRICARE. The annual deductibles for individuals in active duty is $150 and $300 for families. The maximum annual out-of-pocket amount is $1000. You don’t have to pay any enrollment fees if your spouse is still in active duty. You’re not planning on having a baby for at least another year, but still have to get the family plan.

1. If you decide to get the family plan and continue with it for 25 years, how much will you pay monthly? How much will you have paid total?

$25/month

$25*12*25= $7500

2. Say you didn’t get any health insurance because both you and your spouse never had any medical issues in either of your families. But 7 years after your married, you have 2 kids and one breaks their arm during soccer practice. No insurance but you have been putting $100 in savings every month for the past 6 years. The cost of the hospitalization and care for your child totals to $4,200.

Is the amount you have saved enough to pay for the cost? How much in savings will you have left over after the cost is paid?

Yes.

You will have $3,000 left over.

3. Say you did have insurance, but Tricare only covered the cost of x-rays, ER visit, medical treatment, setting, and pharmacy. These are the most expensive costs when it comes to fixing a broken bone. They account for 80% of the total expense.

How much would they cover and how much would you have to pay for?

.8*4200=3360

They would cover $3,360.

.2*4200=840

You would still have to pay $840

Loans

2. Susy wants to buy a car that costs $37,000. She puts a down payment of $5,000. To pay for the rest Susy takes out a loan of $32,000, it’s a 10 year loan with an APR of 6%.

a. How much will she be paying a month?

$355.27

$10,632.40 in interest

b. If she pays an extra $65 how many months will it take her to pay that off?

420.27= .06/12(32,000)

1-(.06/12+1)^-n

420.27(1-(.06/12+1)^-n)= 160

1-(1+.06/12)^-n= 0.38

-0.62=-(1+.06/12)^-n

-.62= -.005^-n

n(-.62)= n(-1.005^-n)

ln(0.62)= -n(ln1.005)

ln(0.62) = -n

ln(1.005)

-95.8=n

It will take her roughly 95.8 months to pay it off.

c. How much interest does she save if she pays the extra money?

$8,261.87 in interest

10632.4-8,261.87=2,370.53

She saves $2,370.53 in interest.